Revenue Recognition Methods: A Complete Breakdown

Revenue recognition methods determine how and when a business records income in its financial statements. While this may sound straightforward, it is one of the most critical areas in financial reporting because timing directly impacts profitability, compliance, and investor confidence.

Under ASC 606, revenue is recognized when control of goods or services transfers to the customer. This shift moved accounting away from simple payment-based recognition toward a structured, principle-driven approach. It ensures consistency across industries and reduces ambiguity in reporting.

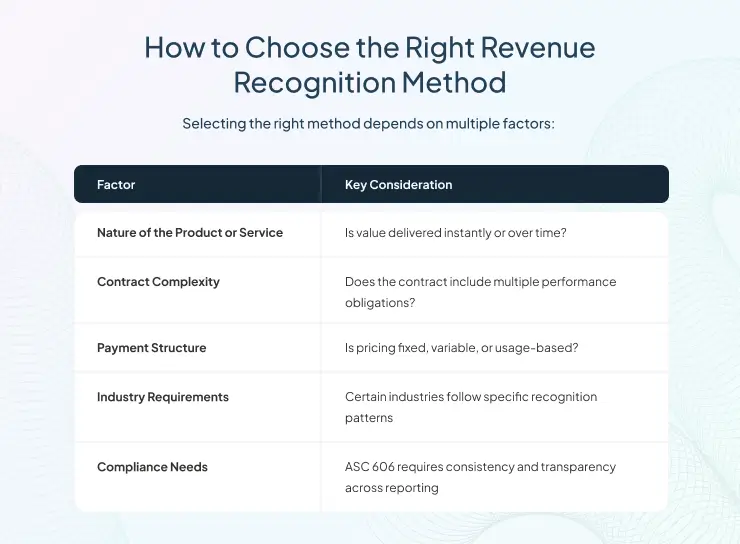

Understanding revenue recognition methods is essential for finance leaders, especially in environments where contracts are complex, services are ongoing, or pricing varies over time.

TL;DR

- Revenue is recognized when value is delivered, not when payment is received

- ASC 606 standardizes recognition across all industries

- Different methods apply based on contract structure

- SaaS and subscription models require time-based recognition

- Incorrect methods can lead to audit risks and compliance issues

What are Revenue Recognition Methods?

Revenue recognition methods are the accounting approaches businesses use to decide when income should appear in their financial statements. This is important because revenue is one of the clearest indicators of business performance, and recording it at the wrong time can affect profitability, compliance, forecasting, and investor confidence. Rather than focusing only on when payment is received, revenue recognition looks at when the business has actually delivered value to the customer.

These methods now operate under the principles of ASC 606, the accounting standard that created a unified five-step framework for recognizing revenue. Before ASC 606, many industries followed their own specialized rules, which often led to inconsistency and confusion. The newer framework brought a more standardized approach by requiring businesses to assess contracts based on performance obligations, transaction price, and the transfer of control.

In simple terms, the focus shifted from “When did we get paid?” to “When did we fulfill what we promised?” That distinction matters, especially for companies that work with subscriptions, long-term contracts, bundled services, milestone-based projects, or variable pricing models.

At the core, every company must answer three essential questions before recognizing revenue:

- What exactly has been promised to the customer?

- When is that promise considered fulfilled?

- How much revenue should be recognized once that obligation is satisfied?

The answers to these questions guide the selection of the appropriate revenue recognition method. They also help ensure that financial reporting reflects the real economic activity of the business, not just the timing of invoices or cash collection.

Discover the simple 8-step checklist to make compliance a smooth, turn-key process

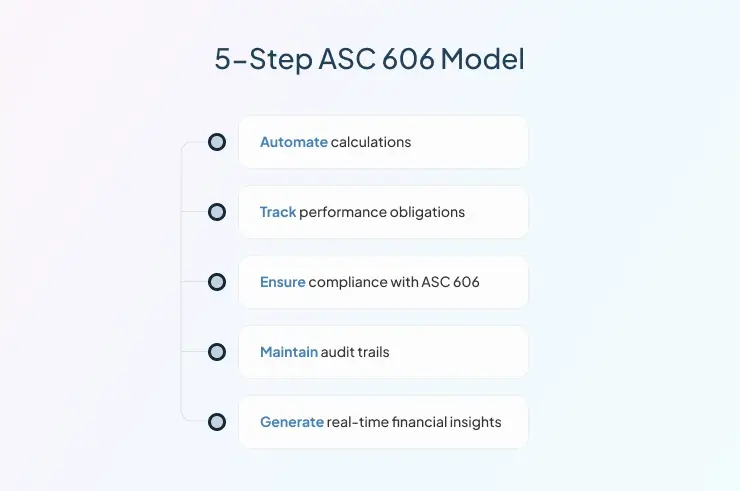

What is the Five-Step Foundation of ASC 606?

Before looking at specific revenue recognition methods, it helps to understand the framework behind them. ASC 606 uses a five-step model to guide how businesses assess contracts and decide when revenue should be recorded. This creates a more consistent and accurate approach across industries.

Step 1: Identify the Contract

The business must confirm that a valid contract exists with the customer. Both parties should agree to the terms, payment conditions should be clear, and it should be likely that the business will collect the payment.

Step 2: Identify Performance Obligations

Next, the business identifies each distinct promise made to the customer. These promises may include products, services, support, training, or other deliverables that need to be evaluated separately.

Step 3: Determine the Transaction Price

This is the total amount the business expects to receive from the customer. It may include fixed charges as well as variable amounts such as discounts, rebates, incentives, or usage-based fees.

Step 4: Allocate the Transaction Price

If the contract includes multiple obligations, the total price must be divided across each one based on its value. This ensures that revenue is assigned correctly to every promised product or service.

Step 5: Recognize Revenue

Revenue is recorded when each obligation is fulfilled. This may happen at one point in time, such as product delivery, or over time, such as in subscriptions or long-term service contracts.

Together, these five steps form the foundation of ASC 606. They help businesses move beyond basic billing events and focus instead on the actual transfer of value, which is the core principle behind modern revenue recognition.

What is the Accrual Method of Revenue Recognition?

The accrual method is the most widely used approach to revenue recognition. It aligns closely with ASC 606 by recording revenue when it is earned, not when payment is received.

How It Works

Revenue is recognized when it is earned, regardless of when payment is received. This ensures that financial statements reflect actual business activity rather than cash flow timing.

Example

A software company delivers a license to a client in March but receives payment in April. Under the accrual method, revenue is recognized in March because the service has been delivered.

Why It Matters

- Provides a true picture of financial performance

- Aligns revenue with related expenses

- Supports better forecasting and planning

Where It Fits

The accrual method is suitable for most businesses, especially those with predictable delivery timelines or contractual obligations.

What is the Cash Method of Revenue Recognition?

The cash method of revenue recognition records revenue only when payment is actually received. It focuses on cash flow rather than when goods or services are delivered. While simple to use, it does not always reflect true business performance.

How It Works

Revenue is recorded when cash is collected, and expenses are recorded when paid.

Example

A consultant invoices a client in March but receives payment in April. Revenue is recorded in April.

Limitations

- Does not reflect when value is delivered

- Often not compliant with ASC 606 for larger businesses

- Can distort financial performance

Where It Fits

Typically used by small businesses or individuals with simple transactions and minimal reporting requirements.

What is the Percentage of Completion Method in Revenue Recognition?

This method is used for long-term projects where revenue is recognized gradually as work progresses.

How It Works

Revenue is recognized based on the percentage of project completion, which can be measured using:

- Cost incurred relative to total cost

- Milestone achievements

- Work completed

Example

A construction company working on a two-year project completes 50% of the work in the first year. It recognizes 50% of the total contract revenue during that period.

Benefits

- Provides real-time financial visibility

- Reflects ongoing performance

- Reduces revenue volatility

Challenges

- Requires accurate cost estimation

- Sensitive to project delays and changes

What is the Completed Contract Method in Revenue Recognition?

The completed contract method recognizes revenue only after a project is fully finished and delivered. It is typically used when there is uncertainty around costs or outcomes during the project. While simple, it delays revenue recognition and can create uneven financial reporting.

How It Works

No revenue is recorded until all performance obligations are fully satisfied.

Example

A contractor completes a project over two years but records all revenue only upon final delivery.

Benefits

- Simple to apply

- Reduces estimation risk

Risks

- Can create uneven financial reporting

- May not align with ASC 606 unless uncertainty justifies it

What is Subscription-Based Revenue Recognition?

Subscription-based revenue recognition records revenue over the life of a subscription rather than upfront. It reflects the continuous delivery of services to the customer. This approach ensures revenue is matched with the period in which value is provided.

How It Works

Revenue is recognized evenly over the duration of the subscription period.

Example

A company charges $12,000 annually for a software subscription. Revenue is recognized as $1,000 per month.

Why It Matters

- Matches revenue with service delivery

- Ensures compliance with ASC 606

- Provides predictable revenue streams

What is Usage-Based Revenue Recognition?

Usage-based revenue recognition records revenue based on how much a customer actually uses a product or service. Instead of a fixed schedule, revenue is recognized as consumption occurs. This makes it common in models like APIs, cloud services, and pay-per-use platforms.

How It Works

Revenue is recognized as the customer uses the product or service.

Example

A cloud provider charges based on data usage. Revenue is recorded as usage occurs.

Key Considerations

- Requires accurate tracking systems

- Revenue may fluctuate month to month

Pro Tip: Always align your revenue recognition method with how your business delivers value. Payment timing alone should never drive recognition decisions.

Real-World Revenue Recognition Examples

Real-world revenue recognition examples help connect accounting methods to actual business scenarios. They show how different models apply based on how value is delivered. Understanding these examples makes it easier to choose the right method for your business.

|

Scenario |

Method |

Recognition Timing |

|

SaaS subscription |

Accrual |

Monthly over contract |

|

Construction project |

Percentage completion |

Based on progress |

|

Product sale |

Accrual |

At delivery |

|

High-risk contract |

Completed contract |

At completion |

|

Cloud usage billing |

Usage-based |

As consumed |

For official standards, refer to the Financial Accounting Standards Board, which governs ASC 606 compliance.

Common Revenue Recognition Challenges

Even with clear standards in place, many businesses still face practical difficulties when applying revenue recognition rules. These challenges often arise from contract complexity, disconnected systems, or inconsistent internal processes.

Misallocation of Transaction Price

When revenue is not distributed correctly across multiple performance obligations, financial results can become inaccurate. This is especially common in bundled contracts where products and services are sold together.

Timing Errors

Recognizing revenue too early or too late can lead to reporting issues and compliance risks. It also affects how accurately the business reflects its actual performance during a given period.

Lack of System Integration

When billing, CRM, and accounting systems do not work together, revenue data can become inconsistent or incomplete. This makes it harder to track obligations, contract changes, and recognition schedules accurately.

Manual Processes

Spreadsheets and manual calculations increase the risk of human error and missed updates. As contract volume grows, these processes become harder to manage and less reliable.

Changing Contract Terms

Contract modifications, renewals, and scope changes often require a fresh review of revenue treatment. If these updates are not handled carefully, the business may apply the wrong recognition method or timing.

Pro Tip: Use integrated financial systems to connect contracts, billing, and revenue recognition. This reduces errors and simplifies audit readiness.

Key Takeaways

Revenue recognition methods form the backbone of accurate financial reporting. As business models evolve, especially with the rise of SaaS and usage-based pricing, applying the right method becomes even more critical. ASC 606 has brought much-needed consistency to revenue recognition, but it also requires businesses to rethink how they approach contracts, pricing, and delivery. Organizations that invest in the right processes, systems, and frameworks are better positioned to maintain compliance, improve financial visibility, and make confident business decisions.

Ready to simplify the path from opportunity to cash?